When to start receiving Social Security retirement benefits is an important decision, especially when you consider retirement could span 20 years or more. That’s where a Social Security split strategy can help.

Many individuals, however, do not maximize their retirement benefits, instead opting to collect early benefits at a reduced rate. One recent study from United Income found that just 4 percent of retirees start their Social Security benefits at the optimal time. So, how should retirees assess when to collect benefits? It’s largely an individual decision. Here are some key considerations for making the best decision for you.

Eligibility & Benefits

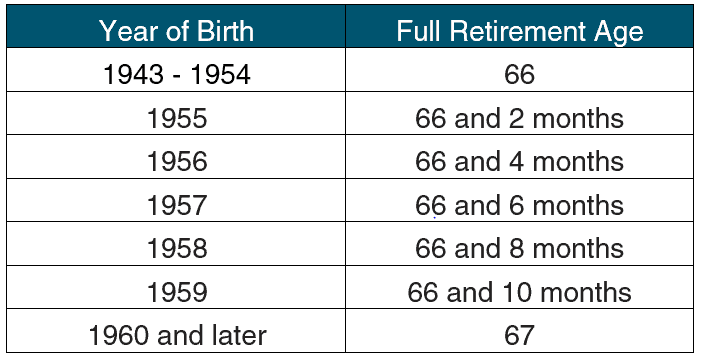

Social Security retirement benefits are generally available to individuals with at least 40 earned credits, which is the equivalent of 10 years of employment. Based on an individual’s earnings record, the Social Security Administration (SSA) calculates a “primary insurance amount” (PIA) which reflects the retirement benefits available at full retirement age (FRA).

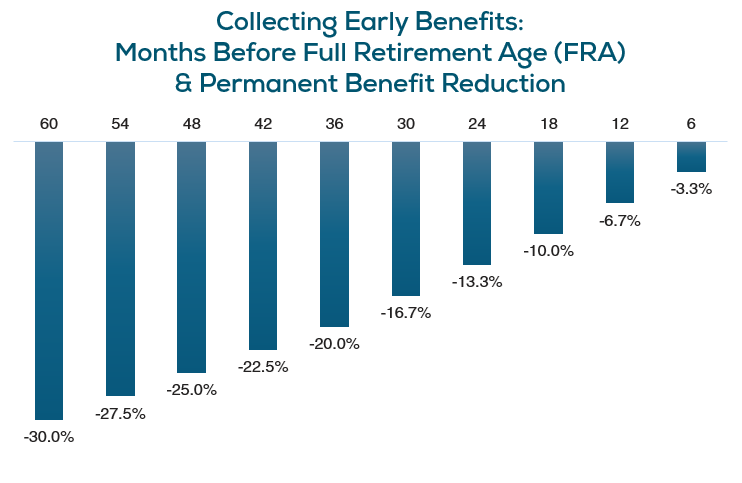

Individuals can choose to collect retirement benefits as early as age 62 or as late as age 70. For those who elect to start benefits before full retirement age, a permanent reduction applies depending on how early benefits are collected.

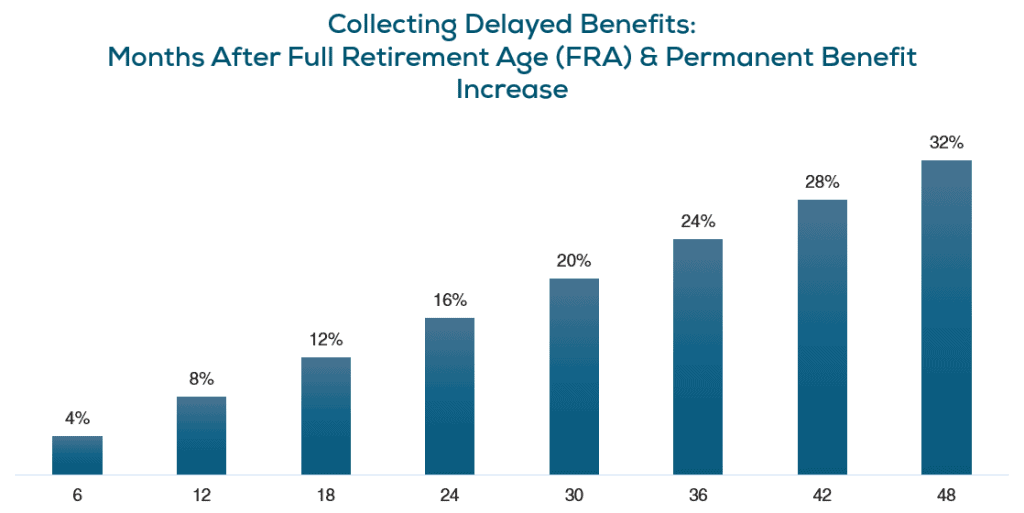

For individuals who wait to collect Social Security retirement benefits, a delayed retirement credit applies. For individuals born in 1943 or later, the delayed retirement credit works out to two-thirds of one percent for each month deferred beyond FRA (an eight percent annual benefit increase), up to age 70. So, for an individual with an FRA of age 67, the FRA monthly benefit could be permanently increased by 24 percent if they waited until age 70 to collect.

Spousal Benefits

Both current and ex-spouses may be entitled to a spousal benefit. While certain rules and restrictions apply, an individual can collect the greater of their benefit based on their own earnings record or 50 percent of the spouse’s full retirement age benefit.

A spousal benefit may be collected as early as age 62 (or earlier if raising a dependent or disabled child), though at a reduced amount. To collect a spousal benefit, the spouse must have already filed to receive benefits (with an exception for divorced spouses). If the primary earner chooses to delay retirement benefits, the spousal benefit is not improved, because it is based on the benefit as of full retirement age.

Other Considerations

We generally advise waiting to collect benefits, but there could be many reasons for a different approach.

Life Expectancy

According to the Social Security Administration, a 65-year-old today has a life expectancy of approximately 19 years for men and 22 years for women. Current health and family health history are critical factors when evaluating an appropriate start date for benefits.

Income Needs

Retirees with sufficient retirement savings may have the resources to delay benefits several years to permanently increase monthly benefits. Given the significance of delayed retirement credits (up to an eight percent annualized improvement), one strategy is to tap retirement savings (IRAs, 401(k), etc.) to bridge the gap while not collecting Social Security benefits.

Survivor Benefits

Couples that are similar in age and with similar benefits may have greater planning opportunities, with the ability to collect one benefit while postponing the other to accrue delayed retirement credits. Survivor benefits are based on the higher-earning spouse’s benefit, so delaying benefits could enhance future survivor benefits.

Current Employment

Individuals that are still working yet choosing to collect benefits before full retirement age may be subject to benefit reductions. Prior to the year of full retirement age, $1 of benefits is deducted for every $2 earned above the annual earnings limit ($24,480 in 2026). In the year of full retirement age, benefits are reduced by $1 for every $3 above the earnings limit ($65,160 for year of FRA). Benefit reductions due to the earnings limit are only temporary, as the monthly benefit will be recalculated upon full retirement age to give credit for previously withheld payments.

Social Security Split Strategy & More

While the “file-and-suspend” strategy ended as of April 2016, there are still other claiming strategies that can be beneficial for couples:

62/70 Split Strategy

Under this strategy, the spouse with the lower earnings records starts benefits between age 62 and full retirement age, while the other spouse (with the higher earnings record) delays benefits until age 70 so they can collect the highest possible benefit. In this situation, if the higher earning spouse who delayed filing until age 70 passes away after age 70, the lower earning spouse would be able to take the higher earning spouse’s bigger benefit and drop their own.

This scenario provides for some Social Security income while enhancing the payout on the higher benefit. More importantly, it may also provide for greater survivor benefits in the future.

If both you and your spouse are in good health, delaying claiming social security until age 70 would help you collect the highest possible payout.

Restricted Application

Individuals that were born before January 2, 1954, and who are at least full retirement age may file a ‘restricted application’ which allows the filer to claim a spousal benefit tied to the lower earner’s benefit while deferring their higher benefit, thus receiving delayed retirement credits. This strategy can be useful for couples where both spouses have notable earnings records and who have the financial resources to forego the higher benefit for a few years.

Other Helpful Resources

Understanding all of the details regarding Social Security benefits can be challenging. Review the resources at your fingertips, like our retirement calculator or Social Security calculator. Reach out to a financial professional so you can get your questions answered and make the best decision for your unique situation on when to start taking Social Security. Try our to estimate your benefits.

Looking for a more in-depth resource? CLICK HERE to request a mailed copy of the 2026 Guide to Social Security.