Employer-based retirement plans provide a powerful mechanism for W-2 employees to reduce their tax liability and save for retirement. But far too often people do not take advantage of this important benefit. The reasons for not participating or under-participating are varied, but many lose out because they imagine using a 401 (k) to be a difficult and complex process. And, based on this assessment, decide it is not worth it and not for them. Others believe there is no benefit to long-term investment. These perceptions is understandable, but are demonstrably incorrect and harmful. Utilizing a 401 (k) is generally straightforward and impactful. Moreover, it generally only requires four decisions:

- Decision #1: How Much to Save?

- Decision #2: Which Contribution Option is Right?

- Decision #3: How to Invest?

- Decision #4: Who Will Be the Beneficiary?

This article is the third in a series and focuses on Decision #3.

Mutual Funds

Generally speaking, the investment options available in a 401(k) plan are mutual funds. There are exceptions to this general rule. As examples, some 401(k) plans will use exchange trade funds, instead of mutual funds. Some will allow the purchase of a company’s publicly traded stock by its employees. Others, generally called 401(k) self-directed brokerage accounts, will allow the purchase of a wide variety of investments, including individual stocks and bonds. But, generally speaking, most 401(k) plans offer a specific selection of mutual funds for participant investment.

A mutual fund is a financial instrument that pools money provided by numerous investors and uses that money to purchase marketable securities, such as stocks, bonds, or money market instruments. Mutual funds are administered by professional fund managers in accordance with the specific investment objectives and methods set forth in the mutual fund’s written prospectus. Some mutual funds are managed passively, e.g., an S & P 500 index fund seeking to match the index’s returns. Others are managed actively, e.g., a mutual fund manager may seek to invest in stocks that she thinks will perform better than the S & P 500 index.

Mutual Fund Styles: Individual Mutual Funds vs. Profile Funds & Target Date Funds

As noted above, mutual funds are administered in accordance with the objectives and methods outlined in their written prospectus. But, generally speaking, within a 401(k) plan, there will be two overarching styles of mutual funds:

Individual Mutual Funds

Individual funds are likely what investors generally hear about in the media and think about when they consider investing. These are a broad swath of funds that can be designed to invest using a wide variety of methods and securities. As examples, they can be passively (index funds) or actively managed and can be designed to invest a wide variety of asset classes, e.g., large capitalization stocks, long term bonds, short term bonds, small capitalization stocks, or the S&P 500 index. Within a 401(k) plan, the menu of individual funds is generally for investment do-it-yourselfers. In other words, investors who want to pick and choose, create, monitor, and adjust their own diverse investment portfolio. Trust Point 401(k) plans offer a wide variety of individual mutual funds for such investors.

Profile Mutual Funds and Target Date Mutual Funds

Profile funds and target date funds generally hold a mixture of underlying mutual funds, stocks, and/or bonds that is set and potentially adjusted over time by a professional fund manager. These styles of investing are generally for people who are new to investing, who are not interested in investing, and who do not have the time or inclination to research individual funds or engage in appropriate asset allocation over time. Generally speaking, a 401(k) plan will include profile funds or target date funds, but not both.

Profile funds generally set a predetermined asset allocation that may or may not be modestly adjusted by the professional fund manager in response to market conditions. A profile fund is generally selected based on an investor’s age and individual risk tolerance and is the single investment vehicle for all of a participant’s 401(k) assets. Profile funds are generally described based on the underlying securities held and the type of returns sought. As examples, Trust Point offers a variety of Trust Point Profile Funds: High Growth, Moderate Growth, Balanced Growth, Conservative Growth, and Fixed Income. The Trust Point Profile Funds engage in asset allocation via underlying mutual funds and seek returns in concert with their titles and prospectus. The Trust Point Profile Funds are subject to modest adjustment by Trust Point’s professional investment team in response to market conditions and in an effort to improve returns.

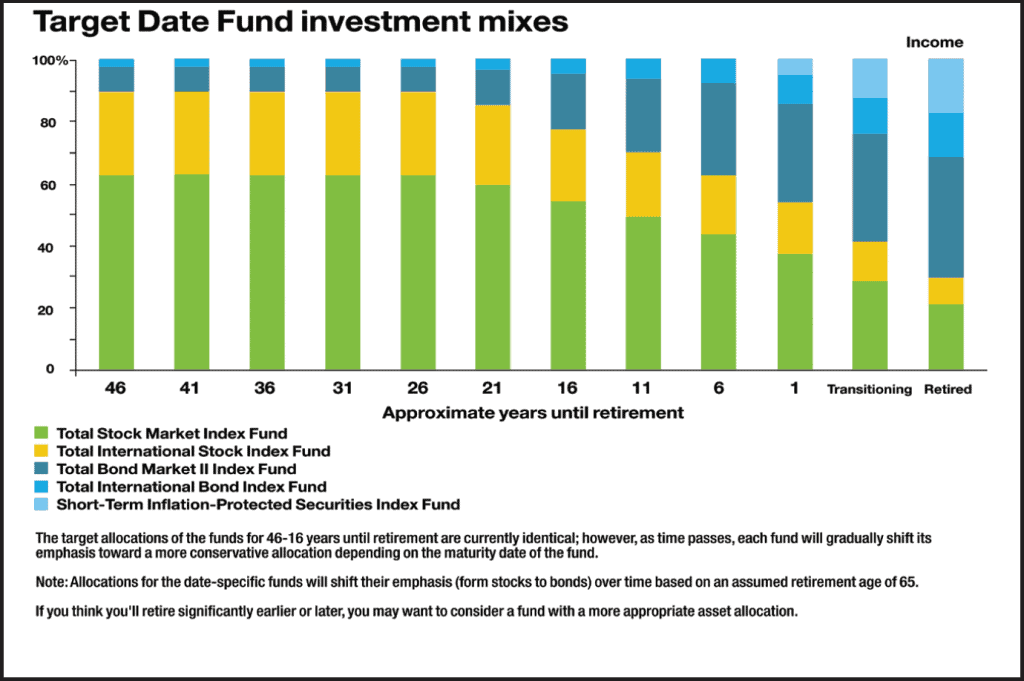

Target date funds are designed to automatically decrease risk over time – by automatically decreasing stock holdings and automatically increasing fixed income and cash equivalent holdings. The “glide path,” i.e., the timing and structure, of this risk reduction is set and based on an investor’s planned retirement date. Thus, generally speaking, all an investor must do using target date funds is choose the target date fund with the date that most closely matches the investor’s planned retirement date and direct all 401(k) assets to that chosen target date fund. Thereafter, the target date fund will automatically adjust asset allocation over time to reduce stock exposure as the chosen retirement date approaches. Trust Point offers a full suite of Vanguard target date funds as an alternative to the Trust Point Profile Funds.

Risk Level, Risk Reduction, and Risk Tolerance

Embedded in the discussion of mutual fund styles are the general concepts of risk level, risk reduction, and risk tolerance.

Generally speaking, stocks are considered to be a riskier asset class than bonds or cash equivalents. But, in part because of the higher risk they carry, stocks generally provide a higher expected return than bonds or cash equivalents.

With this in mind, retirement planners generally suggest reducing the amount of stock holdings in a portfolio – and increasing the amount of bond and cash equivalent holdings – as retirement approaches. In other words, stepping down the staircase of likely risk as retirement approaches.

Of course, not all human behavior is logical. Thus, while retirement professionals may recommend certain levels of risk, and, thus, certain asset allocations, based on a variety of objective variables, one of the most important variables is subjective—an investor’s own, personal risk tolerance. Risk tolerance can be investigated and reasonably measured using a variety of methods, including questionnaires and other testing materials. But, at the end of the day, the best indicator of risk tolerance is an investor’s own prior behavior. If, for example, an investor sold all stock the last time there was a market downturn, it is likely that investor should be very careful about taking on too much risk. If, on the other hand, an investor bought more stock during the last downturn, because stocks were “on sale,” then that investor might be better positioned in more of a high risk, high reward portfolio.

Time vs. Timing: Investing for the Long Term

Time in the market – and a long-term perspective – are critical for a 401(k) investor. Because, generally speaking, the longer an investor is invested in the market, the better that investor can do. Moreover, how soon an investor starts using their 401(k) plan, and how long an investor uses their 401(k) plan, are decisions that – unlike the sometimes wild fluctuations in the stock and bond markets – can be controlled and can make a massive difference in the investment funds available for retirement.

This is best shown by illustration.

In this illustration, Mary starts investing via her 401(k) plan as soon as she starts working. She defers a modest amount that she can afford over the course of ten years – $12,000 total or $1,200 per year or just $100 a month. After ten years she stops investing. For whatever reason – life happens and she needs those funds to pay for it. Despite that, and despite having invested only a total of $12,000, at the end of her working life, she has amassed $211,413 in contributions and projected returns.

Jerry puts off investing via his company’s 401(k) plan. He waits ten years after he starts work before he starts deferring and putting money into the 401(k) plan.

He invests a total of $39,600 over the remaining course of his career. That’s $1,200 per year. But for more than three times as long as Mary.

Because Jerry started later, and thus his contributions had less time in the market, his final account balance comes out significantly behind Mary’s balance. He only amasses $181,473 in contributions and projected returns.

Again, time in the market and a long-term perspective are critical. Importantly, this concept is distinguishable from the notion of “timing the market.” In other words, attempting to getting in and out of stocks and bonds at precisely the right times to increase returns. Generally speaking, timing the market is very difficult, if not impossible, for 401(k) investors. Instead, 401(k) investors require time in the market and should strive to be invested as soon as possible for as long as possible.

Final Thoughts

In general, early, significant, and sustained participation in a 401(k) plan is a powerful way to obtain tax benefits and save for retirement. It can make a real difference in quality of life in retirement and this benefit should be maximized as much as possible. Moreover, how to invest, and what investments to choose, requires careful thought and an accurate assessment of interest, retirement needs, retirement timetables, and risk tolerances.

With all of that in mind, consulting with a trusted and knowledgeable financial professional is always a good idea. But the possibility of some more complexity or analysis in the future should not keep employees from getting involved, participating, and contributing as soon as possible. There are options within most 401(k) plans that limit the necessary decisions and analysis – and provide a meaningful way to get started.

![]()

Author: Jon Marquet

Jon Marquet is the Retirement Plan Consultant at Trust Point Inc. He is a licensed attorney in Minnesota, Iowa, New York, and New Jersey. He works with business owners to identify and address their needs in connection with employer-based retirement plans. He also works in concert with plan sponsors, plan participants, and others in Trust Point Inc.’s Retirement Plan Services group to initiate, administer, and regularly review client employer-based retirement plans. He has presented and written on numerous and various topics throughout his career.