The Tax Cuts and Jobs Act (TCJA) of 2017 made major changes that impact the number of taxpayers who itemize deductions, including increasing the amount of the standard deduction and limiting the amount of state and local income tax (SALT) that an itemizing taxpayer can deduct to $10,000.

The One Big Beautiful Bill Act (OBBBA), passed in July of 2025, made several changes to the TJCA. For example, the OBBBA temporarily increases the SALT deduction to $40,000 for joint filers and from $5,000 to $20,000 for those married and filing separately for tax years 2025-2029. The SALT cap begins phasing down to $10,000 at an income level of $500,000. This might mean that more people are able to itemize again, but the four charitable techniques outlined in this article to support a person’s desire to give charitably may still apply.

1. BUNCHING CHARITABLE CONTRIBUTIONS

A technique that is seeing renewed interest is bunching charitable contributions every other year or even less frequently. In the year that you bunch your charitable contributions, you would plan that your total itemized deductions, including charitable contributions, exceeds the standard deduction. In other years, you would take the standard deduction and not make any charitable contributions.

However, the OBBBA made several changes to charitable giving. There is now a 0.5% adjusted gross income floor. This means itemizers can only get a benefit for itemized charitable deductions over 0.5% of their AGI. Furthermore, there is a limit on overall itemized deductions for taxpayers in the 37% tax bracket. It is important to consult with your tax preparer before using this technique.

This technique can still work well from an income tax planning standpoint but may make it difficult for the charities you support to budget and maintain appropriate cash flow each year. Additionally, this technique requires that you create a monitoring system for yourself to track the years you plan to itemize and match that to the years that you make your charitable gifts.

2. DONOR-ADVISED FUNDS

Another version of bunching is to use a donor-advised fund (DAF) offered by your local community foundation or other providers. Using the DAF method, you would contribute the equivalent amount of money of your normal charitable giving over a number of years and instruct the fund to spread that amount over a period of years to specific charities. You would itemize deductions in the year that you fund the DAF and use the standard deduction in other years.

The advantage of this approach over bunching is that your selected charities continue to receive monies each year. Rather than you making a direct contribution, the DAF makes the annual distribution on your behalf.

3. QUALIFIED CHARITABLE IRA DISTRIBUTIONS (QCDs)

QCDs actually predate the TCJA. If a taxpayer meets the requirements, this is an excellent way to receive a tax benefit for those who are charitably inclined, regardless of whether they itemize.

The regulations allow an IRA holder to make a distribution from their IRA directly to a qualified charitable organization.

Requirements include:

- The IRA holder must be age 70 1/2 or older when the charitable IRA distribution is processed.

- The QCD must be distributed directly from the IRA by the custodian/trustee to the IRA holder’s charity of choice.

- The maximum annual QCD per taxpayer, in total, is $108,000 (as of 2025, indexed for inflation). This limit applies to the total amount of QCDs from all IRAs in a year. A QCD can be done as one large distribution or several distributions from multiple IRAs.

- In the case of a married couple, if both spouses meet the requirements for a QCD, they can each use the technique, which increases the household maximum allowed QCD to $216,000 (as of 2025, indexed for inflation).

Benefits of QCDs include:

- The distribution is not federally taxable (Note: Some states, including both WI and MN, have also adopted QCDs; for residents of those states, the distribution is also not state taxable).

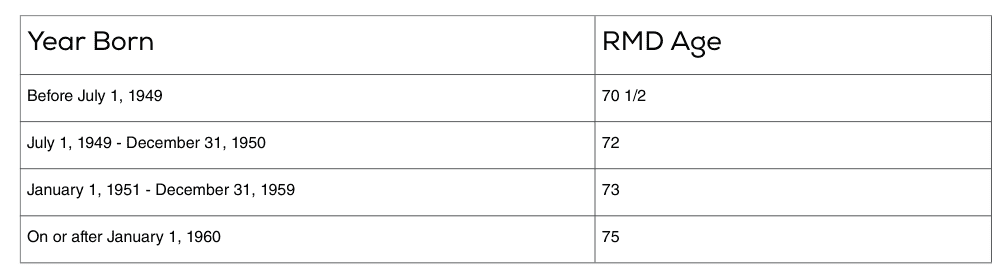

- The distribution counts toward the IRA holder’s required minimum distribution (RMD). NOTE: The SECURE ACT 2.0 changed the starting age for RMD calculations (please refer to the table below for the RMD starting start age based on year of birth). It did not change the age requirement for Charitable IRA distributions, which remains at 70½.

- Distributing all or part of your RMD as a QCD reduces your adjusted gross income (AGI).

- AGI is used to determine social security taxability; lowering AGI may lead to reduced taxable social security benefits.

- AGI is also used to determine Medicare premiums; lowering AGI may lead to reduced Medicare premiums.

Some donations, such as donations to donor-advised funds or private non-operating foundations, are ineligible.

4. NON-ITEMIZED CHARITABLE DEDUCTIONS

Starting in 2026, single filers who do not itemize can deduct $1,000 of cash donations to charity. The limit is $2,000 for married couples filing jointly.

Reach out to a financial professional if you have questions.

For those who are charitably inclined, these techniques can assist you in gaining an income tax benefit. Contact the professionals at Trust Point to learn more about what options are best for you.