Best Defense: Make a Plan and Stick to It

Nearly everywhere you turn, from friends and colleagues to cable news shows, you can find someone with a strong opinion about the financial markets. People will often use specific terms such as correction or bear market to render judgments about the direction of markets, especially when market performance is choppy or trending down.

Is it worth getting concerned when markets stop or even reverse their upward advance?

To answer that, it’s important to realize that downturns are not rare events: Typical investors, in all markets, endure many of them during their lifetimes.

Even knowing this, it can be unsettling to witness the decline of your portfolio during one of these events. After all, that account balance is more than a number—it represents very important personal goals, such as the ability to retire comfortably or to provide a quality education for family members. When market conditions place those goals in jeopardy, you may feel compelled to do something, such as sell most or all of your investments. You may assume that converting to cash will give you a better long-term result than staying invested. But such action would shut you out of the strong recoveries that have historically followed market downturns.

It’s worth noting that not all financial declines are the same in length or severity—for example, historically speaking, the global financial crisis and Great Recession of 2008–2009 was an extreme anomaly. As challenging as that event was, it was followed by the longest stock market recovery in U.S. history.¹

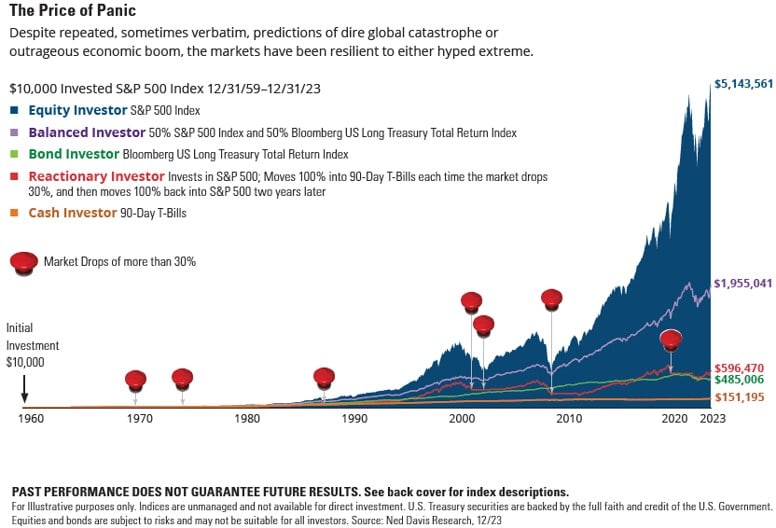

Staying invested is key. As the chart below shows from past performance, long-term investors have been able to rebound from market drops of more than 30% better than reactionary investors.

The Price of Panic Chart

Sources: Vanguard calculations, using data from FactSet. All data as of June 28, 2019.

Chart: For illustrative purposes only. Indices

1 Lu Wang, “The Bull Market Almost No One Saw Coming,” Bloomberg Businessweek, December 15, 2019, https://www.bloomberg.com/news/articles/2019-12-15/the-bullmarket-almost-no-one-saw-coming, accessed on December 19, 2019.