Overview of fiduciary duties and enforcement of the breach of fiduciary duties

Recent headlines concerning the pending lawsuit against UnitedHealth Group for alleged breaches of fiduciary duty in connection with the administration of the UnitedHealth Group 401 (k) Savings Plan1 have many retirement plan sponsors scrambling to better understand their duties, and potential liability, in connection with their 401(k) plans and other employer-based retirement plans. In particular, plan sponsors want to better understand what duties are owed to their plans and plan participants, who owes the duties, and, maybe most importantly, what they can do to limit their potential liability.

Duties Owed By A Plan Fiduciary

The Employee Retirement Income Security Act of 1974 (“ERISA”) imposes a variety of duties on the parties responsible for managing retirement plans. The duties imposed by ERISA are called fiduciary duties and the responsible parties, which always include the retirement plan sponsor, are called retirement plan fiduciaries.

Under ERISA, retirement plan fiduciaries owe the fiduciary duties of prudence and loyalty to plan participants and beneficiaries. They must carry out their responsibilities appropriately and solely in the interests of plan participants and beneficiaries. Retirement plan fiduciaries are also bound to adhere to the requirements of the governing retirement plan documents and to refrain from prohibited transactions.

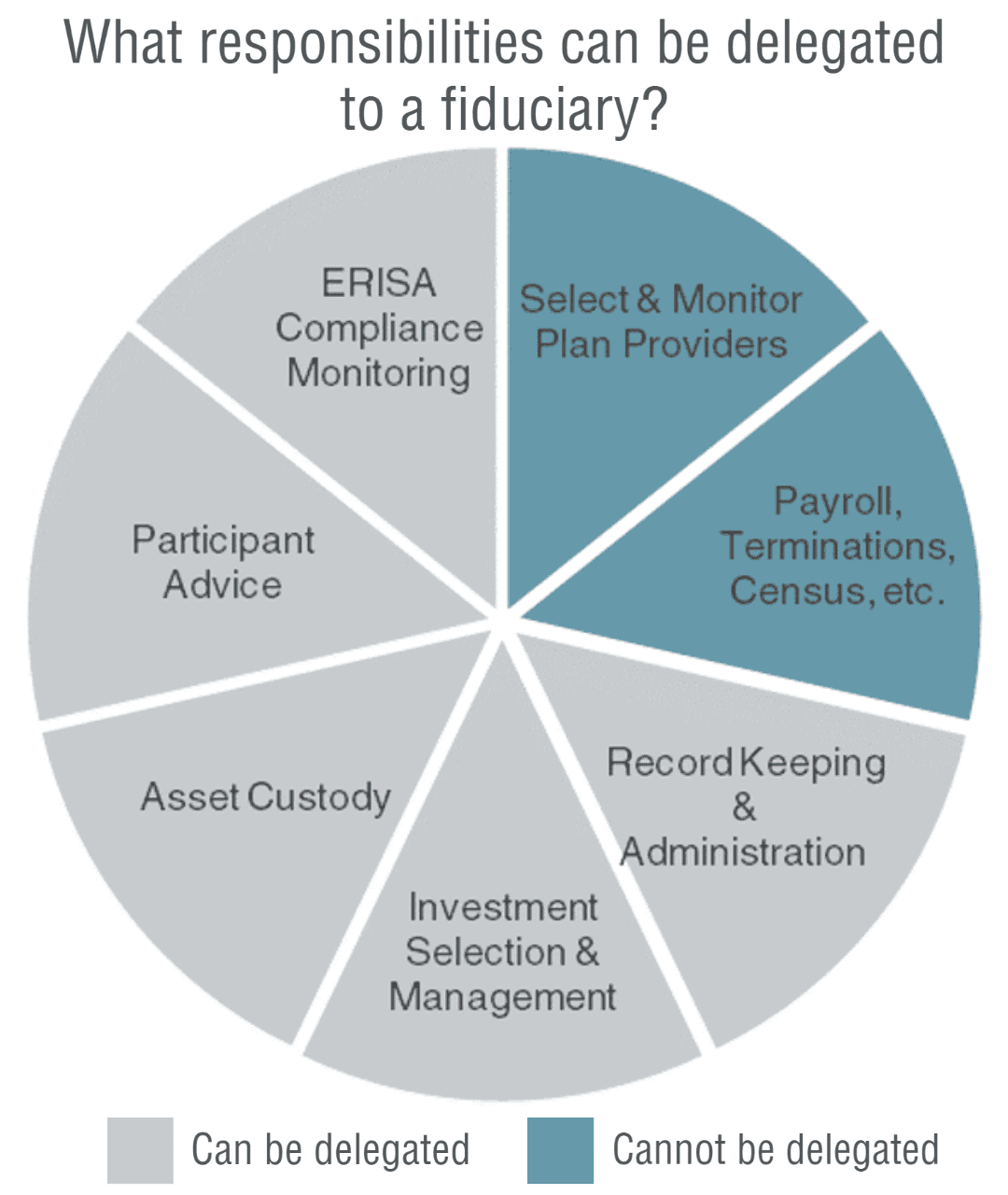

Practically and generally speaking, these fiduciary duties mean that retirement plan fiduciaries must:

- Carefully select and monitor appropriate plan service providers, including to assure that the services provided are necessary and that the costs of those services are reasonable;

- Appropriately administer and coordinate payroll, terminations, and other census data with the plan and plan service providers;

- Engage in appropriate and correct plan recordkeeping and administration;

- Select appropriate plan investment options and engage in continual management and monitoring of plan investment options to assure that they remain appropriate and that inappropriate, or otherwise deficient, options are timely removed from the plan;

- Appropriately custody and securely maintain plan assets;

- Provide appropriate plan and investment-related advice to plan participants; and

- Monitor, understand, and implement all relevant legal requirements, including all relevant ERISA requirements, to ensure that the plan is in appropriate compliance with ERISA, and all other pertinent law, at all times of its operation.

All of these responsibilities must be satisfied by the retirement plan sponsor. However, how this happens, can vary. While some of these fiduciary duties cannot be delegated, many may be delegated by the plan sponsor to an appropriately selected and monitored retirement plan service provider.

For example, while a plan sponsor cannot delegate the requirement of prudently and loyally selecting and monitoring appropriate retirement plan service providers, they can delegate plan investment options, including the selection and continual management and monitoring of the investment options. Moreover, once an appropriate retirement plan sponsor is selected, most of the other fiduciary responsibilities can also be similarly delegated to that service provider.

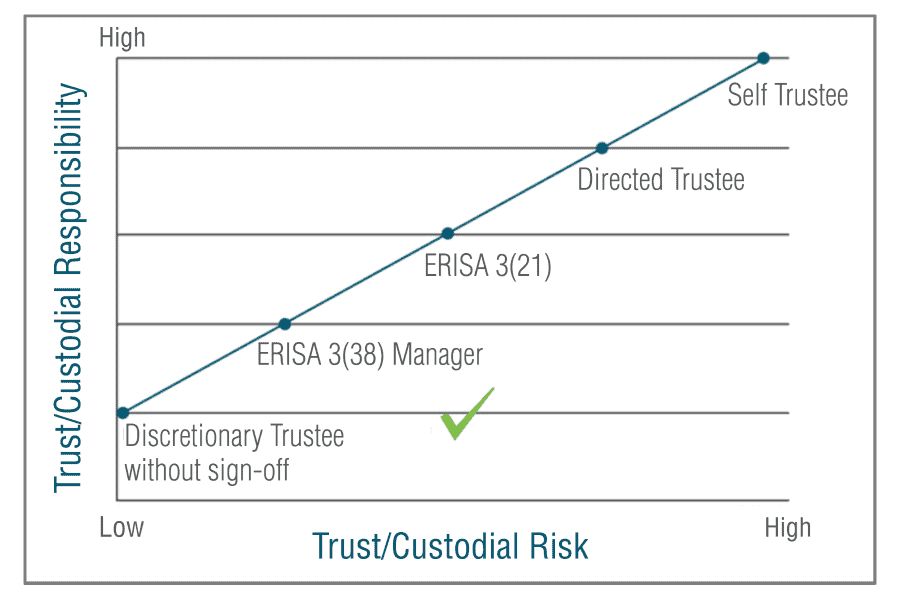

Retirement plan service providers can accept various levels of fiduciary responsibility. Generally speaking, a plan service provider acting as a discretionary trustee without signoff accepts the highest level of fiduciary responsibility – i.e., accepts all fiduciary responsibility that can be delegated under law by a plan sponsor to a plan service provider. There are various other levels of possible retirement plan service provider responsibility and delegation, from sponsors that accept some fiduciary responsibilities, e.g., ERISA 3(21) or 3(38) fiduciaries, down to arrangements where plan service providers accept no fiduciary responsibilities, e.g., a self-trustee arrangement.

Fiduciary duties are significant and place serious requirements and burdens on plan sponsors. Thus, while each potential arrangement might have a place within the universe of employer-based retirement plans, it is important for every plan sponsor to fully and completely understand what fiduciary responsibilities their service providers have – and have not – accepted. Only by understanding the full scope of the arrangement, can plan sponsors ensure that all pertinent fiduciary obligations are being met.

Enforcement of Breaches of Fiduciary Duties

The pending lawsuit against UnitedHealth Group demonstrates how breaches of fiduciary responsibility are generally enforced: civil litigation. In the case of UnitedHealth Group, the plaintiff alleges a wide variety of fiduciary duty breaches, including the retention of underperforming target date mutual funds in an effort to “curry favor with, and benefit, UnitedHealth’s key business partner, Wells Fargo, and advance united Health’s self-interest.”

Civil litigation is the general enforcement mechanism because ERISA makes retirement plan fiduciaries personally liable for any harm caused by breaches of their fiduciary duties [29 U.S.C. § 1109 (a)]:

(a) Any person who is a fiduciary with respect to a plan who breaches any of the responsibilities, obligations, or duties imposed upon fiduciaries by this subchapter shall be personally liable to make good to such plan any losses to the plan resulting from each such breach, and to restore to such plan any profits of such fiduciary which have been made through use of assets of the plan by the fiduciary, and shall be subject to such other equitable or remedial relief as the court may deem appropriate, including removal of such fiduciary. A fiduciary may also be removed for a violation of section 1111 of this title.

Indeed, the last few years have shown a marked increase in ERISA lawsuits alleging the mismanagement of 401(k) and other defined-contribution retirement plans. And many predict this rising litigation trend will continue well into the future for a wide variety of reasons, including the recent U.S. Supreme in Hughes v. Northwestern University.

There, the Supreme Court examined a Seventh Circuit decision that found that because the retirement plan fiduciaries “had provided an adequate array of choices, including ‘the types of funds plaintiffs wanted (low-cost index funds).’…In the court’s view these offerings eliminated any claim that plan participants were forced to stomach an unappetizing menu.’” In doing so, the Supreme Court found that the Seventh Court “erred in relying on the participants’ ultimate choice over their investments to excuse allegedly imprudent decisions by [the retirement plan fiduciaries].” And held that “plan fiduciaries are required to conduct their own independent evaluation to determine which investments may be prudently included in the plan’s menu of options. If the fiduciaries fail to remove an imprudent investment from the plan within a reasonable time, they breach their duty.”

Regardless of the reasons, the apparent increase in litigation in this arena should cause plan sponsors to take stock. Understanding plan sponsor fiduciary responsibilities – and the responsibilities that have been accepted – and not accepted – by plan service providers is a critical first step to avoiding future problems.

With all this in mind, trusted and knowledgeable advisors should be consulted when assessing current or future employer-based retirement plans. And due consideration should be given to engaging a retirement plan service provider that will serve as a discretionary trustee without signoff and that will therefore accept the highest level of fiduciary responsibility that plan sponsors can delegate.

[1] See, e.g., https://www.startribune.com/lawsuit-alleges-unitedhealth-group-mismanaged-investment-options-in-worker-retirement-plan/600202048/; https://www.minnpost.com/glean/2022/08/lawsuit-unitedhealth-group-mismanaged-retirement-plan-investment-options/. (News links last visited on October 6, 2022.)