Finances are a common cause of frustration for couples, but there are ways to keep money from making a mess of your marriage. Even the most blissful couples aren’t immune to marital challenges, and at the top of the list for many is managing money.

After marriage, financial habits that once only affected an individual suddenly impact the lives of two people and more if children enter the picture. How money is spent, how it’s saved, financial priorities—these things can vary widely from person to person and aren’t always discussed before vows are exchanged.

And sometimes even the wealthiest couples can’t avoid these conflicts. In fact, more money often leads to more marital problems. But money struggles don’t have to be a deal-breaker in the relationship.

Communication is key for overcoming most financial woes and spouses need to work together to develop a long-term financial plan that both can agree on. Whether you’re about to be married or have already walked down the aisle, here are some key considerations for that important discussion.

Money Management: Topics to Discuss

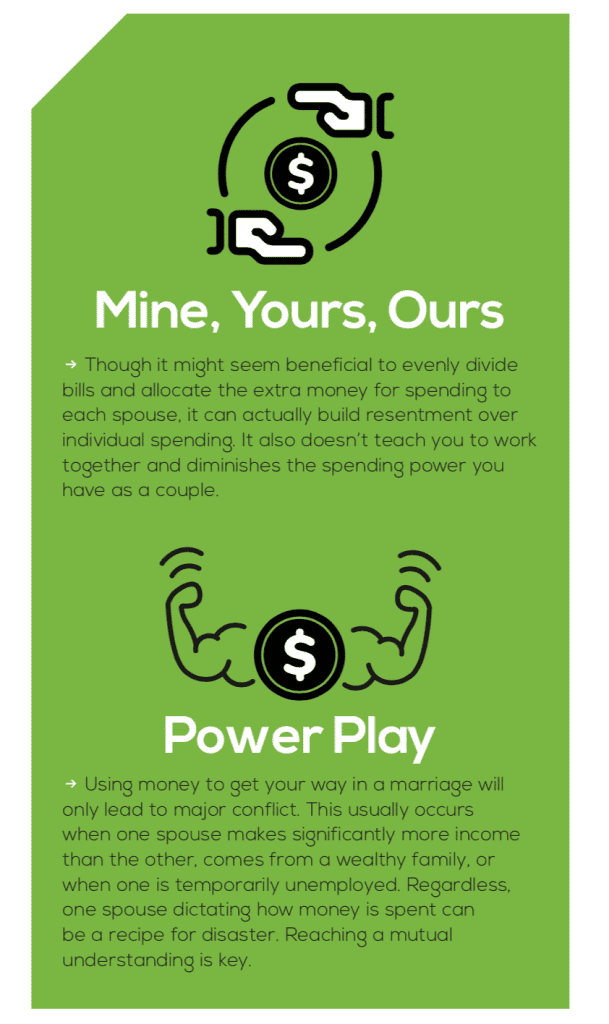

Financial control can be one of the stickiest subjects that a married couple will face. There are many ways a couple can manage its finances, and there is no right or wrong answer, but it’s imperative that both individuals agree on their level of involvement.

Here are some essential topics to discuss:

- Goals – Define your short-term (0-3 years), mid-term, and long-term (10+ years) financial priorities as a couple.

- Budgeting & Cash Flow – Build a joint budget that outlines your income, fixed expenses, and variable spending.

- Credit & Debt – Commit to monitoring your credit together.

- Insurance – Review life and health insurance needs.

- Bank Accounts – Decide whether to merge accounts, maintain separate ones, or use a combination of both.

- Taxes – Determine whether filing jointly makes sense for you, as it may provide benefits like higher standard deductions and tax credits.

- Retirement Planning – Assess how your marriage impacts retirement and pension accounts, and align on long-term savings strategies.

- Estate Strategy – Update your will, healthcare power of attorney, and other key estate documents.

Where you land on all of these questions will depend on each person’s comfort with that part of the finances. Some people want to have complete control and visibility for every cent that comes in and out, and some people would prefer to have nothing to do with it.

Make sure that you have a conversation about each of the questions above, and that you know who will be in charge of what. Poor communication, especially about finances, can put a lot of strain on an otherwise successful marriage.

Existing Loans and Debts

The existing debts and loans that you each owe are one of the most important aspects to consider before marriage. Most people of typical marrying age and some that are marrying later in life will likely have one or several of the following kinds of debt: student loans, car loans, personal loans, and credit card debt.

Most debt belongs to the individual who originally borrowed it unless you have a co-signer. However, while you may not legally be “on the hook” for your partner’s debts, once you become married, each of your loan responsibilities will impact your joint household, which affects you both.

Make sure that you have an open and transparent conversation about all forms of debts in each other’s name, and what the plan is to repay it on time. Your debt-to-income ratio as a couple could play a significant role in getting a mortgage or other type of loan and especially in getting the best interest rates.

Family Support

The biggest discussion in this area is probably whether to have children. Though many factors go into that decision, from a purely financial perspective it can cost upwards of $300,000 to raise a child to the age of 18.

Beyond children, couples might need to support other family members in one way or another. Regardless, have a plan and communicate about it often. Be open and honest with one another and be sure to listen to your partner to understand their perspective.

Whether you have children or not, you should probably discuss tax and estate planning with a financial professional to make sure you are on the right track and can accomplish all of your goals.

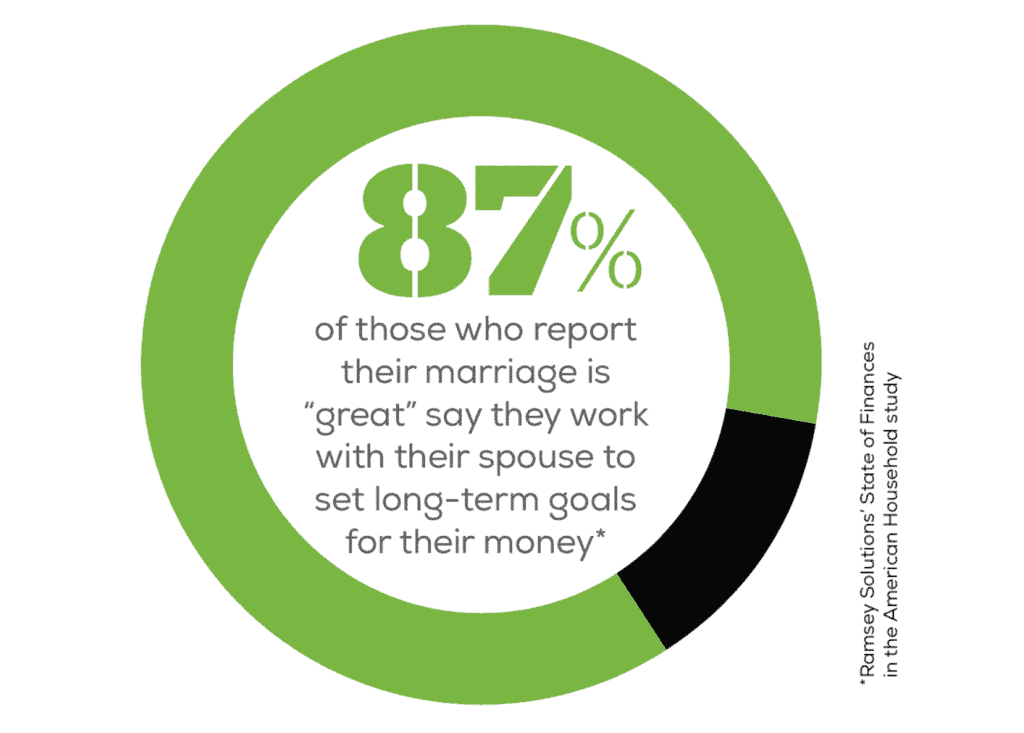

Reaching Long-Term Goals

Marriage is fundamentally a partnership between you and your significant other. To make it a successful partnership, you need to make sure that the two of you are on the same page regarding your financial goals.

Are you both individually and collectively on track to retire comfortably? If not, how will you plan to get back on track? We’ve already discussed debt, but it should be a primary goal to make debt payments manageable and have a good plan toward paying it off.

As you begin to build wealth, you should also consider what your long-term plans are for investing that money. Create common goals and determine what kind of investment will not only get you there but also one where you are both comfortable with the risk level. It’s important you and your partner agree on the direction you’re working toward.

Prenuptial Agreement

We saved the most awkward topic for last. While in the moment it seems as though your relationship will last forever, the stark reality is that somewhere between 40 percent and 50 percent of marriages in the U.S. end in divorce, according to the American Psychological Association.

Without an agreement in place to dictate how assets are to be defined and divided, a breakup can lead to significant legal disputes around your current and future finances. Especially in cases where one individual is bringing significant financial assets to the table, it might make sense to put a prenuptial agreement in place to ensure that there is a fair financial settlement in the event that the relationship doesn’t work out in the long run. If you’re afraid to have this conversation when things are going well, think about how difficult it will be if things are going poorly.

Here to Help

Getting married is a significant life event that should bring joy, comfort, and happiness. But it also brings with it a host of financial decisions that are important to consider. Take heed, use these tips, and money matters won’t have to come between you and your happily ever after.

And remember, Trust Point can help. Whatever stage of life you are in, we take the time to listen to your values and customize a plan that is just right for you.

When the Marriage Ends

Going through a divorce or losing a spouse is never easy. The process can be messy, stressful, and frustrating.

After things have settled and you start getting back into a routine, you still have to deal with handling your finances on your own. Historically, this challenge more commonly affects women. According to a report from global wealth management firm UBS, women are living longer than their husbands, yet 56 percent of women leave financial and investing decisions to their husbands. And regardless of the circumstances, eight out of every 10 women will eventually be solely responsible for handling their own finances.

At Trust Point, we work alongside you to help you make the right financial and investing decisions and to make sure we continue to meet your financial objectives and feel secure in your future. Here are our top tips if you find yourself in sole control of your finances, maybe for the first time:

Get started right away, but wait to make big decisions.

It’s natural to be stressed out at the thought of trying to manage your day-to-day life after a significant life event. The key to staying in control is being assertive and confident when it comes to managing your finances. To do this, take an inventory of your assets and know what your cash flow needs are so that you have a better understanding of your situation. You may feel pressured and rushed to start making financial decisions. Slow down. Take your time. When it comes to these decisions, the best practice is to think through all of them.

Find a trusted financial advocate.

One way to alleviate the pressure you feel is to recognize that this isn’t something you need to go through on your own. Don’t try and get through it solely off of advice from friends and family. Trust Point financial professionals are experts when it comes to situations like this. There are a lot of details that are easy to overlook when it comes to getting your finances in order after a marriage ends, such as closing joint accounts and opening new ones, changing beneficiaries on insurance policies or wills, creating a new estate plan, and more.

Create a budget and stick to it.

If you had any joint accounts or were liberal in terms of spending one another’s money during your marriage, then you need to learn to budget with the money that you make. If you don’t have much experience with budgeting, here are three things to keep in mind when creating your first budget:

- Identify why you want to create a budget. In this case, it is to be able to find financial freedom while learning to adjust to a single income household.

- Do a deep dive into current spending habits. What are you spending the most money on per week? What is necessary spending, and what are expenses that you can try and cut back on?

- Determine your financial goals. Do you still want to retire at a certain age, or assist your kids in getting through college? Create some measurable goals that will motivate you to stick to your budget.

Financial planning and budgeting may seem intimidating at first, but most people find out that the process is actually quite enjoyable, as it gives them a new sense of control over their wealth.

Invest wisely.

Investing your money is a great way to gain more financial freedom.

If you’re sitting on extra cash in your account after a financial settlement following your divorce, it’s smart to hang onto it for the short term until you’ve adjusted to your new lifestyle. But at some point, you may want to invest your money to help preserve and increase your wealth to help reach the financial goals that you’ve created.

When it comes to smart investing, you need to construct the right portfolio that takes into consideration how much money you will need to support your lifestyle, as well as the amount of risk you’re comfortable with. At Trust Point, our investment professionals can help mitigate various risks, including market risk, interest rate risk, inflation risk, and more.

Investing can be intimidating for some, but at Trust Point we will customize your plan and educate you along the way to ensure you feel confident in knowing where you stand and what you need to do to reach your goals.