Saving money comes easier to some than others. Good money management means having the discipline to consistently put money aside and save vs. spend, in order to stay on track with your financial goals. Whether you are a consistent saver or need some help putting funds away for retirement, there is always room to do more. This is especially true for your 401(k). Before we jump into the different ways to make additional contributions, let’s first discuss the current regulations for 401(k)s.

Current 401(k) Regulations

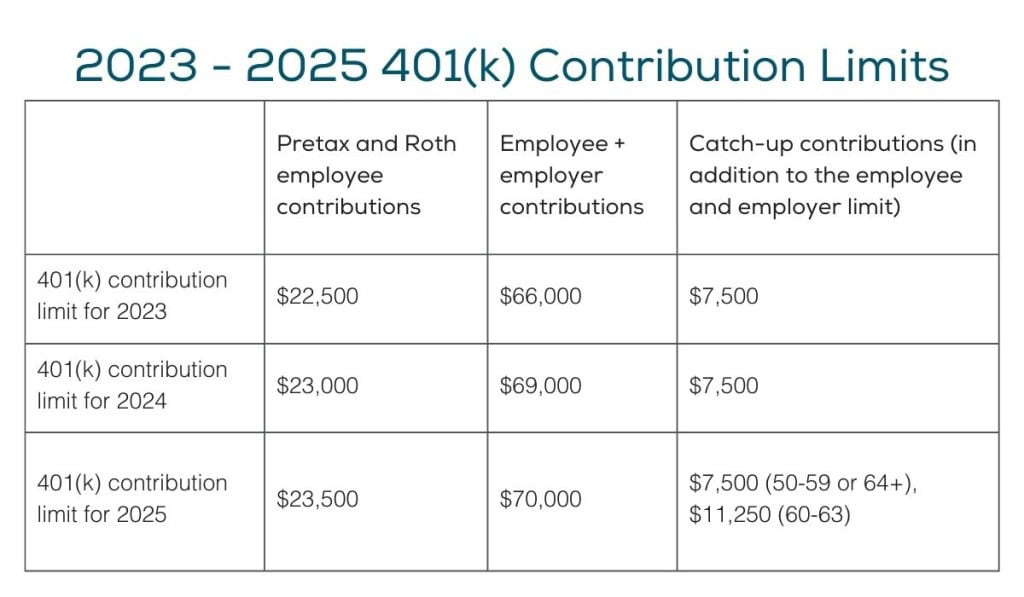

For 2025, the contribution limit for employees who participate in a 401(k) is $23,500. Those aged 50 to 59, or 64 or older are eligible to contribute and additional $7,500 in catch-up contributions. Beginning in 2025, those between ages 60 and 63 are eligible to contribute a catch-up contribution up to $11,250. These numbers also apply to other saving avenues, like a 403(b), most 457 plans, and the federal government’s Thrift Savings Plan.

Please note, if you have multiple 401(k) accounts, you are still limited to contributing the total employee contribution amount of $23,500 between all your plans.

Please note, if you have multiple 401(k) accounts, you are still limited to contributing the total employee contribution amount of $23,500 between all your plans.

3 Ways to Make Additional 401(k) Contributions

If you believe that you need to start making some additional contributions to your 401(k), here are three options to consider:

Year-End Bonuses

Year-end bonuses are actually a great way to add to your 401(k). Supplemental pay, like bonuses, are typically subject to a higher withholding rate compared to your regular pay. Employers will usually either use a bonus tax rate of 25%, or they will combine the bonus with an ordinary paycheck and then withhold tax using traditional tax tables. So, no matter which way your employer operates, you’ll see a higher rate of tax withholding.

To avoid this scenario, you can request that your employer make a larger 401(k) deduction from your bonus. If you take this approach, the money is placed into your 401(k) where it won’t be taxed until you retire. Keep in mind, this money is still subject to the annual contribution limits for a 401(k).

Increase Your standard 401(k)

Those who save up every nickel and dime that comes their way understand how small changes to help increase their savings can be crucial to meeting their goals for retirement. These small savings add up over time and can make a huge difference to your 401(k) down the road. You can increase the amount currently set aside for your 401(k) by as little as one percent, and that small increase will certainly add up. Pump up your contribution rate each year by increasing it by one to two percent. The best time to do so is when you get a wage increase or pay off a loan. That way, you won’t feel the impact on your pocketbook as much. It especially makes sense if you’re in your 50s, due to the contribution limit being higher than when you’re under 50-years-old.

Check out Trust Point’s Retirement Calculator to see how even the slightest increase in your standard contribution set aside in each paycheck can benefit you in the long run.

After-Tax Contributions

One of the less popular ways to make an additional contribution to your 401(k) is to do so with an after-tax contribution. This can be beneficial particularly in cases where expected tax rates in the future are projected to increase.

After-tax contributions are exactly what they sound like – when you make a contribution with money that’s already been taxed. An important thing to remember about these contributions is that you must claim these contributions on your income tax return for the year in which they were made. So, as the taxpayer, you may be entitled to a refund based on your contributions at the going tax rate.

There isn’t much incentive to add money to your 401(k) this way that’s why people don’t typically make this type of contribution. The additional money put towards your 401(k) is not tax-deductible, like it would be when it comes directly from your paycheck. However, once these after-tax contributions are made, they accumulate investment income on a tax-deferred basis. Therefore, these contributions will not only allow you to have more money when you retire, but you’ll also have the option to retire earlier, if that is your goal.

These benefits can make after-tax contributions enticing for some.

Work with a Financial Professional

As an employee, it is important that you take full advantage of the retirement plan options available from your employer. No matter if you’re a young professional just starting work, or someone nearing retirement, the more you know about your finances, the better your chances of reaching your goals. At Trust Point, we provide you with the tools you need to maximize the benefits from your retirement plan.

We know that planning for retirement can be stressful, and we want to help lessen this burden by helping you create a concrete plan that will leave you confident and prepared for the future, no matter what it holds for you. Contact Trust Point today for assistance with your financial planning!